Sovereign Gold Bonds of Government of India – a risk factored evaluation

Draft (email comments to tirumalakv@gmail.com)

Brief

Unconventional monetary instruments carry risks that need to be quantified to help policymakers make an informed decision by allowing an objective cost-benefit analysis.

This paper discusses Sovereign Gold Bonds (SGBs), a unique monetary instrument issued by the Government of India, and quantifies the risk that the government bears while underwriting the guarantee on the future gold price. One way to quantify this risk could be by using Black-Scholes-Merton’s option valuation model. It is seen that quantified risk arrived this way outweighs potential benefits arising from cheaper money raised through SGBs. This helps policymakers to understand the true risk they are undertaking by promising future gold price-linked returns.

Sovereign Gold Bonds (SGBs)

Sovereign Gold Bond (SGB) scheme was launched in November 2015. The main objective of SGB is to act as an alternative to purchasing/holding physical gold. These bonds are issued on payment of Indian Rupees and is denominated in grams of gold. The bond returns the Indian Rupees equivalent to the same number of grams of gold at the time of maturity. The bond has a maturity period of eight years. Bonds are issued on behalf of the Government of India by the Reserve Bank of India (RBI) and have a sovereign guarantee. The bonds are restricted for sale to resident Indian entities. The investment limits are presently 4 kgs per fiscal year, for individuals and Hindu Undivided Family (HUF) and 20 kgs per fiscal year for Trusts and similar entities. The ceiling will be counted on a financial year basis and will include the SGBs purchased during the trading in the secondary market. The ceiling on investment will not include the holdings as collateral by Banks and Financial institutions. Interest payable on these bonds is half-yearly @ 2.50% percent per annum. Interest on the Bonds is taxable as per the provisions of the Income-tax Act. The bonds are available both in demat and paper form and are tradeable in the Secondary Market. The capital gains tax arising on redemption of SGB to an individual has been exempted. The indexation benefits will be provided to long terms capital gains arising to any person on transfer of bond.

(Technical details on SGBs may be found at Appendix C. FAQs on the SGB scheme: https://m.rbi.org.in/scripts/FAQView.aspx?Id=109).

Series of SGBs are released multiple times every year to the public for subscription. There is no specified upper value on the amount released for subscription, and the public can subscribe as per the eligibility guidelines when the series opens for subscription. The SGB subscription has grown significantly in the last two years, indicating that the bond is gaining traction with the public.

Financial year (April-March) | Issue value in Rs. Crore | Issue value in USD million (1USD=75 rupees) |

2015-16 | 245 | 32.7 |

2016-17 | 4553 | 607.1 |

2017-18 | 1895 | 252.6 |

2018-19 | 643 | 85.8 |

2019-20 | 2316 | 308.8 |

2020-21 | 16049 | 2139.8 |

2021-22 (till Nov) | 11088 | 1478.4 |

Table 1: Subscription to SGBs over years – Data from RBI

Gold import countermeasures

| Year | Value in USD Billion | |

| 2001 | 4.8 | |

| 2002 | 3.7 | |

| 2003 | 5.4 | |

| 2004 | 8.8 | |

| 2005 | 11.7 | |

| 2006 | 13.3 | |

| 2007 | 17.2 | |

| 2008 | 19.9 | |

| 2009 | 23.4 | |

| 2010 | 38.4 | |

| 2011 | 53.7 | |

| 2012 | 52.6 | |

| 2013 | 37.7 | |

| 2014 | 31.0 | |

| 2015 | 35.0 | |

| 2016 | 22.9 | |

| 2017 | 36.1 | |

| 2018 | 31.9 | |

| 2019 | 31.2 | |

| 2020 | 21.9 | |

| 2021 (Jan-Nov) | 51.1 | |

| Source - Trademap for all years except 2021. For 2021, source is DGCIS data | ||

Figure 1: India's gold import over years

Comparison of SGB and Treasury Bonds

Gold price risk in SGBs

While raising money through such unique instruments, the issuer bears the associated risks and should suitably price the instrument to account for such risks. If the government is the issuer, then such risks are ultimately borne by taxpayers and citizens unless they are nullified. In the case of SGBs, the gold price is anchored to the bond value at the time of issue. Gold price fluctuation is a risk which the government bears. In case of significant price appreciation of gold between the time of issue and maturity, the initial gains of the government may turn into losses. On the other hand, a drop in gold price may lead to additional gains for the government.

One possible strategy to counter gold price risk could be to purchase equivalent amount of physical gold as a hedge, when the government issues the SGBs. However, this would be counter to the objective of the SGB – which aims to act as an alternative to purchasing/holding physical gold. Government would also incur storage and security costs on such physical gold. Additionally, government would incur a cost of 2.5% per year that is paid out as interest. Therefore, this strategy is not optimal. This paper therefore assumes that government doesn’t undertake any gold purchase to offset gold price risk.

Central banks around the world buy gold for forex management and other purposes. RBI too buys/sells Gold for central banking/forex management purposes. It is not linked to SGB. SGB is a debt instrument issued by RBI on behalf of Government of India, which is a separate function of RBI under its responsibility as the public debt manager for the government. Thus, it is assumed for this paper that any fluctuation of gold assets in the forex reserves basket of RBI is also not to be linked to potential SGB hedging activities of the government.

Risk quantification for SGB

Government earns an interest differential when it raises money through SGB over regular sovereign bonds. The yield on regular sovereign bonds of 8-years maturity is over 6 percent (based on yield curve), and such bonds would be listed for auction with annual coupons of around 6 percent. The annual coupon payout on SGB is 2.5% per annum. The differential of over 3.5% is the potential gain for the government when it chooses the SGB route to borrow from public. This potential gain comes with the gold price risk. One possible approach to quantify this gold price risk would be to treat SGB as a risky asset and use hedging techniques to arrive at the valuation for the underlying risk.

We shall take a simple approach and compare whether the gains arising out of raising money through SGB outweigh the quantified risk. We may use a standard similar-maturity sovereign bond for comparison. A sovereign bond has no risk for the purpose of our calculations. The mechanics would involve arriving at the gains coming from borrowing money using SGB over a standard sovereign bond, and checking if this compares well with the risk involved.

Let’s assume that an SGB worth 1000 crore Rupees (10 Billion Rupees) is issued at the same time as a sovereign bond of the same par value with a similar maturity period (8 years) during a reference year, say late 2021. The sovereign bond gives coupons, paid out semiannually at 6.1% per annum rate, until maturity and pays out the par at maturity along with the last semiannual coupon. The SGB on the other hand pays 2.5% interest per annum, paid semiannually, and let’s assume for now that it also pays out par value at maturity along with the last installment of interest. The assumption of payout of par value (Rs. 1000 crore) at the time of maturity is to make the comparison with sovereign bonds easier. If this plays out in real, the SGB would be a better way to borrow money from the public as the interest rates to be paid on SGB is far lesser than that on a standard sovereign bond. However, the last par value payout on SGB might not be Rs 1000 crore, but it can be more or less than Rs 1000 crore depending on where the gold price prevails at the time of maturity. This risk is what we quantify now.

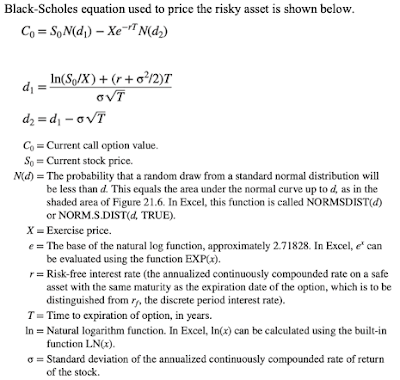

The gold price risk for the Government can be modeled as the price for writing a European Call Option maturing in 8 years at a price equal to the current value which equals the assumed par value that is paid out at maturity. The assumption is that the call buyers (public) would encash the option at any price, but from the SGB issuer’s point of view, any payout above par value is the gold price risk that is being borne over and above that of a normal sovereign bond. The call writer thus bears the risk of any upward movement in the price of Gold beyond the existing price. This paper uses the Black-Scholes model to arrive at the call price for the European Option. One may also model Black’s equation for the European future Option in this case. As the value for a European future Option and European Call Option contract maturing at the same time is the same for both Black and Black-Scholes models, this paper shall use Black-Scholes.

The SGB gold price risk modeled as a European Call Option is justified on the basis that SGBs are usually redeemed at maturity upon completion of eight years. While there is an option to list and trade the SGBs on secondary exchange from the fifth year onwards, it is noticed that the liquidity of SGBs is extremely limited and most of the bonds are kept in the custody of investors and redeemed at maturity. This assumption may come under challenge once the SGB market develops further, and we may then need to revise the calculations to an American-type Option. However, for now, we may use the assumption of European Call without losing accuracy.

(Appendix B - calculations and formulae for Black-Scholes and Black’s model)

The calculation has the following steps:

Step1: Calculate the present value of all payments over eight years for a normal government bond.

Step 2: Calculate the present value of all payments over eight years for an SGB.

Step 3: Find the difference between the present value of payouts at Step 1 and Step 2. This would give us the gains the government derives from issuing an SGB over a normal bond of eight-year maturity.

Step 4: Calculate the price of writing a European Call Option with a strike price equal to the current price of gold. This is the quantified gold price risk.

If the quantified value of risk at Step 4 is larger than the value arrived in Step 3, it means that the policymakers need to justify the additional price paid to raise money through SGB.

The risk-free rate for Option price calculation

Black Scholes model uses the risk-free rate to discount for the present value of the future strike price of the Option. The current analysis relies upon the existing bond return rates on similar-maturity duration bonds (by interpolating the rates if required), to arrive at the risk-free rate (Appendix A). As the government of India has never defaulted on its obligations, this paper considers the government bond rate for a similar duration (8 years) as practically risk-free for the purpose of estimation.

The risk-free rate thus comes out to 6.1 % for an 8-year maturity bond.

The standard deviation of Gold prices for Option price calculation

The standard deviation (sigma for Black-Scholes) has arrived from the historical estimation of fluctuation in gold prices in INR.

Three different annualized standard deviations for the returns are calculated to generate three scenarios:

· Standard deviation for the returns covering period over 40 years from 1979 to mid-December 2021. The prices on a weekly basis are used to calculate the annualized log-returns and standard deviation. The standard deviation for this period comes to 0.189.

· For the period covering 8 years ending in mid-December 2021. The standard deviation for this period comes to 0.141.

· For the period covering 3 years ending in mid-December 2021. The standard deviation for this period comes to 0.152.

These standard deviations look reasonable when compared against implied volatility in the gold futures market. For long-term gold futures ending in December 2026, the implied volatility is around 17.15% (link). Thus, the standard arrived to generate the scenarios using historical data appears to be erring on the conservative side.

Calculations and findings

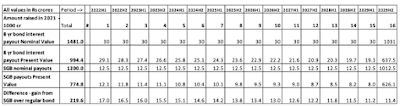

a) Benefit from issuing SGB over normal bonds

Differential gain arising due to coupon and par value payouts between regular bonds raised at risk-free rate of 6.1% with a semi-annual coupon payout of 6% per annum versus SGB raised at 2.5% per annual coupons paid out semi-annually is shown below.

The government gains a total of 219.6 crore rupees measured in terms of present value (discounted at risk free rate) by issuing an SGB of Rs 1000 crores in place of a standard eight-year bond.

|

| Comparison calculation of SGB vs Normal Sovereign Bond |

b) Price to write the call option

The Black-Scholes equation is used to price the call option. The amounts required to write the Call option depends on the scenario using the Standard Deviation. The values in Rupee crores for a strike price of Rs 1000 crore are as shown below:

Standard deviation | 0.189 (40 yr) | 0.141 (8 yr) | 0.152 (3 yr) |

Call option value/Quantified risk (in Rs Crores) | 426.6 | 402.5 | 407.6 |

Finding

Conclusion

The main objective of SGBs is to act as an alternative to purchasing/holding of physical gold.

It is for the policymakers to now examine if this level of risk underwriting is acceptable after examining the impact of SGBs on gold import over years and the gold purchase pattern of the public.

Appendix A

Appendix B

Appendix B

Black-Scholes equation used to price the risky asset is shown below.

Appendix C

SGBs are unique instruments, prices of which are linked to commodity price viz Gold. SGBs are also budgeted in lieu of market borrowing. The calendar of issuance is published indicating tranche description, date of subscription and date of issuance. The Bonds shall be denominated in units of one gram of gold and multiples thereof. Minimum investment in the Bonds shall be one gram with a maximum limit of subscription per fiscal year of 4 kg for individuals, 4 kg for Hindu Undivided Family (HUF) and 20 kg for trusts and similar entities notified by the Government from time to time, provided that (a) in case of joint holding, the above limits shall be applicable to the first applicant only; (b) annual ceiling will include bonds subscribed under different tranches during initial issuance by Government and those purchased from the secondary market; and (c) the ceiling on investment will not include the holdings as collateral by banks and other Financial Institutions. The Bonds shall be repayable on the expiration of eight years from the date of issue of the Bonds. Pre-mature redemption of the Bond is permitted after fifth year of the date of issue of the Bonds and such repayments shall be made on the next interest payment date. The bonds under SGB Scheme may be held by a person resident in India, being an individual, in his capacity as an individual, or on behalf of minor child, or jointly with any other individual. The bonds may also be held by a Trust, HUFs, Charitable institutions, and universities. Nominal Value of the bonds shall be fixed in Indian Rupees on the basis of simple average of closing price of gold of 999 purity published by the India Bullion and Jewelers Association Limited for the last three business days of the week preceding the subscription period. The issue price of the Gold Bonds will be ₹ 50 per gram less than the nominal value to those investors applying online and the payment against the application is made through digital mode. The Bonds shall bear interest at the rate of 2.50 percent (fixed rate) per annum on the nominal value. Interest shall be paid in half-yearly rests and the last interest shall be payable on maturity along with the principal. The redemption price shall be fixed in Indian Rupees and the redemption price shall be based on simple average of closing price of gold of 999 purity of previous 3 business days from the date of repayment, published by the India Bullion and Jewelers Association Limited. SGBs acquired by the banks through the process of invoking lien/hypothecation/pledge alone shall be counted towards Statutory Liquidity Ratio. The above subscription limits, interest rate discount etc. are as per the current scheme and are liable to change going forward.

(Adopted from RBI’s website: https://rbi.org.in/Scripts/FAQView.aspx?Id=79, dt: Jan 4, 2022)

Comments